|

Emergency Management Organization

Flood Resilient Guide for Homeowners

Download the Guide

Flooding and Manitoba Homeowners

Flooding is the most damaging natural disaster in Manitoba.

Flooding applies to all Manitobans, not only those near a river or lake. The provincial and federal governments have invested hundreds of millions of dollars in mitigation infrastructure, including the Red River Floodway, Portage Diversion, Shellmouth Dam and Reservoir, and multiple community dikes. These investments have greatly reduced flood risks but have not eliminated them.

Using the information and checklist in this guide, homeowners can better understand their flood risks and make informed choices to protect their homes.

The Manitoba government or anyone employed with or approved by the Manitoba government assumes no responsibility or liability for any loss or damage that any person may sustain as a result of the information in, or anything done or omitted through reliance on this pamphlet; including any personal injury or bodily injury, including death, and any loss or damage caused by flooding to insured or uninsured structures and/or property where flood resilient principles recommended in the guide have been applied.

Understanding Home Flooding

Types of Flooding

River flooding occurs when the water in a river, lake, or stream overflows its banks, damaging buildings, roads, and lands.

River flooding is common during spring snowmelt or heavy rainfalls. In Manitoba, spring floods are often forecast weeks in advance.

What are Floodplains?

Floodplains are low‑lying areas next to streams and rivers which have experienced repeated flooding.

Over thousands of years, floods deposited soil and nutrients creating flat areas ideal for farming and communities. Properties in floodplains face higher flood risk.

Flash flooding happens when heavy rainfall overwhelms local drainage systems. As a result, you may see water pooling in fields, streets, and underpasses.

Flash floods can happen quickly and there may not be much time for warnings. While rainfall is the most common cause of flash flooding, it can also be caused ice jams or by the failure of dikes or dams.

Coastal flooding occurs near the coasts of oceans or large lakes. Water rises past the shoreline and into communities and homes, often brought on by storm surges from intense winds. Storm surges occur when strong winds push water towards a coast, raising water levels.

While these floods are typically associated with oceans (such as in Northern Manitoba along Hudson Bay), coastal flooding from storm surges also occurs around large lakes like Lake Winnipeg and Lake Manitoba.

Insurance is available for many types of home flooding. Residential overland flood coverage is offered by many insurers and is typically combined with sewer backup and groundwater seepage coverage. A typical home insurance policy will not cover damage due to leaks or seepage over a long period of time. Talk to your insurance representative and ask what coverage you have and what is available. You can also shop around with other representatives. Don't be caught paying out of pocket!

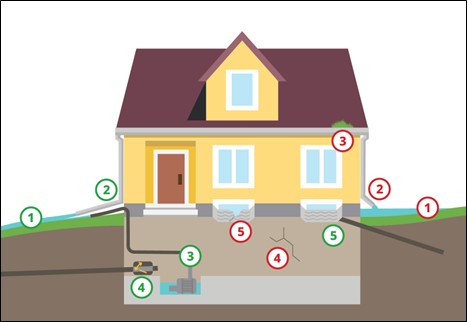

Main Forms of Home Flooding

Many Manitoban cities and towns have areas that combine the sewers that drain water off roads and those that collect wastewater from homes. Combined sewers, then, are sewers that are connected to your home and to rain and snowmelt management infrastructure.

When there is intense rainfall or flooding, rain can fill up the combined sewer and cause that water to make its way back up the pipes to homes. If your home does not have a backwater valve, the water can flow out of your sewage line and into your home.

Sewer backup flooding can also occur in non-combined sewers through blockages, pipe failures, or lack of capacity.

Overland flooding occurs when there is an excess of rain or snowmelt, and the resulting water begins to cover land that is normally dry. As the water builds up, it can find its way into homes through windows, doors, and cracks.

The soil around your home acts like a sponge that can absorb water when it rains. If the soil absorbs more water than it can hold onto, it can release that water. If a building has cracks in its foundation, the soil may release water into the building through these cracks.

Seepage can occur quickly and be obvious, but it can also be slow, releasing smaller amounts of water behind walls and under flooring that damages your home over time.

Natural disaster damages are increasing. In Canada, nine of the ten highest years for insured severe-weather losses have occurred since 2011.

One of the major drivers of this increase is that growth and development have resulted in more infrastructure vulnerable to damage. There are more homes, more businesses, and more roads. There has also been development in high-risk areas, such as along streams which regularly flood nearby homes.

There are also factors that have increased the amount of water that we are seeing. Climate changes over the past 50 years has led to about 7% more precipitation in winter and spring, leading to more spring flooding. It is expected these climate change trends will continue. Changes are also occurring to the land, such as urban sprawl leading to more runoff from concrete surfaces. There is also rural and agricultural land drainage which reduces the natural water storage capacity on the landscape.

Manitoba is seeing more water and more development, but much of our flood and storm sewer infrastructure was built several decades ago. Provinces and local governments are investing in mitigation projects, but it is difficult to adapt existing infrastructure to current best practices.

Understanding Flood Mitigation

Flood mitigation is taking actions to reduce the impacts of flooding, such as:

- Reducing damages to homes

- Reducing stress and disruption during floods

- In extreme cases, protecting lives

Why Manitobans Should Invest in Flood Mitigation

In 2018, the Insurance Bureau of Canada found that it costs an average of $43,000 to repair a flooded basement. But there are many projects under $500 that can greatly reduce a home's risk of flooding.

Homeowners should take action to protect their investments and their home. Page 9 lists low or no-cost mitigation projects. Page 10 begins a section to help you target larger mitigation projects and goals. Many projects only take a few hours or days to complete and can be done by homeowners or contractors. These projects will help reduce the impact of floods and reduce the financial burden of flood repair.

Home Flood Resiliency Examples

Flood Resilient

Flood Vulnerable

1. Talk to Your Local Government

Visit your local government's website or contact them to ask flood-related questions such as:

- What advice can they offer?

- How can you report flooding to them?

- Which flood resilient renovations require a permit?

- Is there funding available for flood mitigation projects?

- Do they know your flood vulnerability such as sewer and storm drain capacity?

2. Insurance for Overland Flood Coverage

Do you have overland flood insurance on your home policy?

Overland flood insurance is not regularly included and is often an additional cost. If you do not have overland flood insurance, check if your insurance broker offers this coverage for your home. Also check to see if you have coverage for sewer backup and groundwater seepage.

If your insurance broker does not offer the flood coverage that you need, shop around for other insurance brokers or carriers that do provide it.

3. Create a List of Items in Flood-Prone Areas

Go through low-lying areas of your home and create a list of items. This will help you file claims if home flooding occurs. Taking a video of your belongings can also help.

4. Home Inspections for Flooding

Have a home inspector help you to identify water damage, how water has entered your home, or how it would be able to enter your home. Home inspectors can also help identify solutions.

5. Consider Your Property's Flood History

Ask previous homeowners, neighbours, and insurance brokers about on flooding history. This will give you a stronger understanding of the risk your property has. You can also ask your neighbours what they have done to help with their home flooding.

Are You Renting?

Depending on local residential tenancy requirements, it may be the property owner's responsibility to address any problems. Even if you can't undertake mitigation projects yourself, you can still reduce impacts of flood damages by keeping your valuables and important documents out of the basement or raised off the floor. See the next page for low or no cost projects.

Below are some additional methods that can be used to improve your resilience to flood damages. These steps will help protect your property and personal belongings from excess flood water while also improving the safety of your home during floods.

- Raise basement electronics and furniture off the ground to protect them from damage.

- Avoid storing valuable and personal items in basements or place them in watertight containers with lids to protect them from damage in the event of water infiltration.

- Clear eavestroughs of leaves and debris twice a year to allow proper drainage.

- Review your home insurance policy for flood coverage. Consider shopping around if your insurance provider does not offer coverage for overland flooding, sewer backup, or groundwater seepage.

- Look into the climate and natural environment risks that you face on your property. Understand what can be done to reduce potential damage and increase resilience.

- Clear sewer drains on your street of leaves and ice, and work with your local authority to clear persistently clogged drains.

- Never pour fats, oils, or grease down your drain.

- Create or refresh your emergency and first aid kits. For information on emergency preparedness and what to include in your kits, visit gov.mb.ca/emo/guide/individuals/before.html

Targeted Mitigation Projects

This targeted project checklist can help you determine the most appropriate flood resilient projects based on your home's history. Find the headers that match your experience and consider the projects below.

Each project has a series of dollar signs to help indicate the relative cost of different projects.

Before starting any projects, homeowners should contact their local authority to ensure all by-laws and construction codes are adhered to.

Cost Estimates

$ = Less than $200

$$ = $200 to $1,000

$$$ = $1,000 to $4,000

$$$$ = $4,000 to $15,000

$$$$$ = More than $15,000

-

Have your sewer line inspected using a closed‑circuit television (CCTV) line

$$

- Identify if your sewer line is in good condition, properly sloped, clogged, or collapsed.

-

Install a backwater valve in the sewer line exiting the property to prevent back‑flooding from storm sewers

$$$

- If you have water entering your home through your basement floor drains, your main sewer lines exiting your home are likely overwhelmed.

- If you have a backwater valve, remove any obstructions and repair the valve.

- Redirect or extend downspouts at least 2 meters from your home $

-

Use an epoxy injection kit to seal the cracks

$$

- Epoxy injection kits force a sealant deep into cracks.

-

Waterproof your home foundation from the outside

$$$$$

- Waterproofing requires excavating soil around your foundation, coating your foundation in waterproofing materials, and then replacing the soil.

- Redirect or extend downspouts at least 2 meters from home $

- Repair and waterproof window/door frames $

- Install or repair window well drains $$

-

Regrade soil around your foundation

$$$

- Soil should slope away from the home.

- Foundation should remain at least 4 inches exposed.

- Redirect or extend downspouts at least 2 meters from your home $

-

Seal any gaps between a sidewalk and your home

$

- Shifting homes and sidewalks can create narrow but deep gaps.

- Gaps can be filled with crushed gravel and polymeric sand.

- Repair eavestroughs that are damaged or not functioning properly $$

-

Regrade the soil around your home foundation

$$$

- Soil should slope away from the home.

- Aim for at least 6 inches of drop over 10 feet.

- Leave at least 4 inches of foundation exposed.

-

Create an urban rain garden

$$$

- Rain gardens collect and redirect surface water.

- Often include native plants and decorative rock.

-

Install an external electrical service disconnect $$$

- Allows power to be disconnected without accessing panels that may be underwater.

-

Raise electrical service equipment $$$$

- An electrician raises the service box above the flood hazard level.

-

Install a flood alarm $

- Flood alarms in basements and garages quickly alert you to water.

- Allows time to react and remove valuables.

-

Install Ground Fault Circuit Interrupters (GFCIs) in the basement $$

- Stops power immediately when water is detected.

- Helps prevent shocks, burns, and short circuits.

-

Purchase and install a backup battery for your sump pump $$

- Power outages often occur during storms when sump pumps are most needed.

-

Install a sump pump and collection basin $$$

- Moves water from a sump pit under your home to the outside.

- Repair your sump pump if it is not functioning properly.

-

Replace regular building materials with water‑resistant materials $$$

- Includes vinyl flooring and replacing lower drywall with PVC trim boards.

- Install a culvert grate to reduce blockages $$

- Excavate silt buildup from the culvert $$

-

Install beaver fencing $$$

- Beaver gates or deceiver fencing reduce blockages while allowing coexistence.

-

Install a larger culvert $$$

- May require permits and licenses.

-

Raise the soil around your foundation $$$

- Pack and seed soils so water slopes away from the home.

- Use clay as a water barrier and topsoil to support grass.

- At least 4 inches of foundation must remain exposed.

-

Purchase and store flood‑preparation materials $$$

- Includes vapour barrier, sandbags, and other water‑stopping materials.

-

Install a ring dike $$$$$

- Packed clay barrier surrounding your property.

-

Relocate your home $$$$$

- Move to higher ground or a less flood‑prone parcel.

-

Elevate your home $$$$$

- Permanently lift the structure above flood height.

After a Flood

Returning to your home or community after a disaster can result in feelings of sadness, grief, or anger. Mental stress can add a burden to physical recovery. It is important to understand that floods don't just affect us physically, but also mentally. Coping with stress can be as much of a disruption as the physical results of a flood event.

The following are some steps individuals can take to prepare for mental and emotional recovery after a disaster:

- Acknowledging your feelings can help you recover from traumatic events. Discuss your worries, feelings, and fears with others close to you and seek professional help with mental recovery as soon as possible.

- Identify and locate community resources and organizations that assist with handling mental and emotional health issues brought on by disaster. This can include organizations such as the Canadian Red Cross and Kids Help Phone.

- Contact your family doctor or other general practitioner regarding issues of stress, anxiety, and other mental health issues.

- Do not enter your home until officials and inspectors say it is safe.

- Ensure that electricity to the property is turned off (normally located in the property electrical panel, circuit breaker box, or fuse box).

- Use caution when entering areas that were flooded. Watch for debris and other hazards that may still exist.

- Ensure anyone entering flooded areas is wearing appropriate protective clothing, including waterproof gloves, heavy‑soled rubber boots, and a dust mask. This can protect you from mold, chemicals, and contaminants.

- Avoid damaged or downed powerlines, utility poles, and cables.

- Follow public health guidelines on safe cleanup and disposal of debris and hazardous materials.

- Make sure that food and water consumed at the flood site are clean and not contaminated.

- Try to identify the causes of flooding so that vulnerabilities can be addressed in the future.

| Item or Document | Who to Contact if Damaged or Lost |

|---|---|

| Animal Registration Papers | Municipal office or veterinary office |

| Banking Books | Bank branch |

| Birth Certificates | Manitoba Vital Statistics Branch |

| Bonds | Bank of Canada - Unclaimed Properties Office |

| Children's services and social assistance identification cards, medical or social assistance cheques | Your assigned case worker |

| Credit cards | Issuing credit card company |

| Documents of immigration | Immigration, Refugees and Citizenship Canada |

| Divorce papers | Court of King's Bench where the divorce was granted |

| Driver's license and vehicle registration titles | Manitoba Public Insurance |

| Income tax records | Canadian Revenue Agency |

| Indian status card | Indigenous Services Canada |

| Insurance policies | Insurance agent |

| Land titles or deeds | Teranet Manitoba |

| Manitoba health card | Manitoba Public Health |

| Marriage Certificate | Manitoba Vital Statistics Branch |

| Medical records | Family doctor or specialist |

| Métis citizenship card | Manitoba Métis Federation |

| Military discharge papers | Veterans Affairs Canada |

| Money (damaged or destroyed) | Bank of Canada Branch |

| Passports | Service Canada |

| Social Insurance Number (SIN) card, Canadian Pension Plan (CPP) documents, and employment insurance documents | Service Canada |

| Stocks | Issuing company or lawyer |

| Will and last testament | Family or estate lawyer |